What Is An Assumable Mortgage?

Table of Content

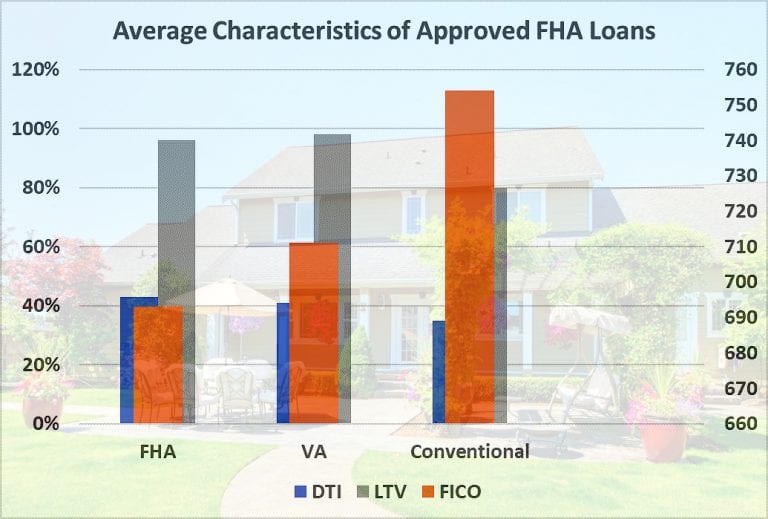

Basic entitlement is $36,000, and the VA guarantees up to four times the entitlement amount, or $144,000, of the loan against default. This acts as protection for the lender, especially if the homeowner is required to move as part of their military service. Generally speaking, lenders will require minimum credit scores of 580 to 620 to qualify for a VA loan. If a borrower has sufficient residual income, some lenders will even approve VA loans with credit scores as low as 500. Mil-to-mil couples can also split their VA loan entitlement evenly for a VA home loan.

A buyer will need to bring the difference ($75,000) to closing. VA home loans also typically require a .5% funding fee of the loan balance from the buyer. For the new buyer to qualify for VA mortgage benefits, they must meet specific requirements. When you assume the mortgage in this manner, the original homeowner is no longer in charge of making timely payments, so it is the best way to acquire the mortgage. The new borrower the person assuming the loan is in exactly the same position as the person passing it on.

How to Assume a Mortgage

If sellers can offer a mortgage at a lower interest rate to buyers, the savings could be substantial and cost sellers nothing. A simple mortgage assumption completely leaves the lender out of the negotiation, transferring payments between seller and buyer without lender consultation. The seller takes on all of the mortgage liability to the lender, meaning that if the buyer defaults on payments, the seller is still responsible for paying the money back to the lender.

For example, your deceased parent may have left you a mortgaged home. When a mortgaged home is inherited, the mortgage's due-on-sale clause prevents the loan from being assumed. However, relatives inheriting mortgaged homes, such as the adult children of deceased parents, can also assume their mortgages if they intend to live in those homes. The death of a parent ranks high on the list of life's most stressing events. When a parent dies, a seemingly endless list of things need to be done. For example, the adult children of a deceased parent with a mortgaged home will need to address any existing home loan.

Assumable Mortgage Pros And Cons

Lenders often have special assumption arrangements for surviving family members if a borrower dies. Simple assumptions are exceedingly rare except sometimes for family transactions. You may be willing to accept the risk if the person taking on the mortgage is, say, your spouse, son, or daughter. But in most situations, a simple assumption is too risky to make sense. Note, however, that your second mortgage will likely come from a different lender than the one that owns the mortgage you’re assuming.

While assuming a VA home loan can be a great option for both borrower and seller, assuming the loan in the wrong way can affect your credit score and VA loan entitlement. VA home loans were introduced in 1944 as part of the GI Bill of Rights Act to ease the transition from military to civilian life. They come with a long list of benefits like no downpayment requirements and lower interest rates. You may need to be prepared to take out a second home loan to cover the difference between the purchase price and what the seller owes on the original mortgage.

How Much Can I Mortgage My House For

Germain, you won't need to refinance your deceased parent's mortgage or even assume it. Just notify your deceased parent's mortgage lender that you're inheriting your parent's home, will be living in it, and will be making the mortgage payments. After inheriting your parent's home, you might need to obtain a new deed in your own name.

Here are some of the lender’s requirements you must meet to qualify for the assumption. In addition to requesting the release of liability, you must also formally substitute their entitlement for yours. If not, your entitlement could be tied to their mortgage, preventing you from borrowing another $0-down mortgage. In addition to being creditworthy, the lender also makes sure that the new borrower agrees to assume all loan liabilities and obligations, including repaying the VA in case of a claim.

The buyer can then substitute their entitlement for the seller's. In such a case, the VA restores the seller's full entitlement. Whether you are the buyer or seller of the home, think very carefully before entering into a loan assumption agreement.

An assumable mortgage allows the buyer to purchase a home by taking over the seller's mortgage loan. Contact the current lender to request assumption information. Even though you are taking over the loan, the lender may require a down payment.

However, assuming a VA loan requires you to pay only 0.5% as processing fees. With the VA loan assumption, you don’t need to apply for a VA loan. This makes your work easy and streamlines the application procedure. This can also prevent you from paying high closing and appraisal fees. This is the most recommended way to assume a mortgage, as the original homeowner is no longer responsible for timely payments.

Mortgages remaining from the 1980s likely have double-digit interest rates that will not compare to the low rate one can get today. An assumable mortgage allows a buyer to take over a seller’s home loan. Not all loans are assumable — typically just some FHA and VA loans are assumable. Most USDA loans are assumable in this manner, which transfers responsibility for the mortgage debt to the buyer but also adjusts the debt by reamortizing it with new rates and terms.

You do not need to visit a regional office for approval if your lender has automatic authority. However, if this is not the case, you would have to seek the lender’s permission and the VA to assume a mortgage. Here are the pros and cons that come with assuming a VA mortgage. Additionally, transferring the mortgage liability to another party can be beneficial for a person moving and leaving their home behind. You can also opt to assume a VA loan in case of a divorce, and you wish to keep the home’s remaining equity. In this article, we’ll discuss everything you need to know about the VA loan assumption.

Additionally, if the buyer has the potential to add a large down payment to the current loan, the lender may be more likely to allow the assumption of the loan. However, a bank may be willing to allow you to assume a mortgage if the current owner is in a financial bind that jeopardizes the payback of the note. Another advantage of having an assumable loan is that it can serve as an incentive for homebuyers, especially if the existing interest rate is low and the terms are particularly good. This can be used as an added selling point if you encounter a buyer who's willing to make a significant cash contribution. For complex situations, it may be in everyone’s best interest to consult with a real estate attorney.

Her articles have been published in the Florida Today and Orlando Sentinel. She earned a Bachelor of Science in Interdisciplinary Studies from the University of Central Florida. Bankrate follows a strict editorial policy, so you can trust that were putting your interests first. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy. Before you try to assume your family member’s mortgage, you should research what type of mortgage it is. Imagine its now January 2023, and you want to assume that mortgage.

In fact, the FHA states that, Assumptions without credit approval are grounds for acceleration of the mortgage, which means the buyer can lose the property to foreclosure. When VA loans are assumed, it’s the servicer’s responsibility to make sure the homeowner assuming the property meets both VA and lender requirements. While VA loan assumption can help a spouse take over the liability of the loan from the veteran, it might not be the best option. If the loan is assumed by a civilian spouse during a divorce, the veteran/service member cannot opt for the release of liability. While assuming the loan, you are required to pay a small closing fee of only 0.5% of the loan amount. As opposed to a traditional home purchase a VA loan allows you to let someone else assume your interest rates, monthly payments, and balance, assuming they qualify for the loan.

Comments

Post a Comment